Offline and feature phone-based payments and targeted payments are the next big charters for the Reserve Bank of India and the National Payments Corporation of India (NPCI), to promote the adoption of the central bank-backed digital currency (CBDC), said two bankers knowing about the matter.

Both the RBI and NPCI want CBDC to make digital payments as simple as cash transactions, the bankers said.

The RBI has also opened a sandbox for startups to test several CBDC use cases. As of now, daily transactions remain in the range of tens of thousands against the target of 1-million-plus, which was expected by the end of December.

“The problem is that CBDC does not solve anything that is not already done by Unified Payments Interface (UPI), which is why it is difficult to get customer adoption,” said the founder of a major payments fintech startup.

Industry insiders believe that as new use cases open up on CBDC, it will attract more users to these wallets.

A unique aspect about the digital currency is that it can be programmed for specific purposes. This opens up massive opportunities in direct benefit transfer, cash spending for specific purposes or something as simple as giving pocket money to children only to be used for a grocery meal or something specific.

“Currently, banks do not have the necessary infrastructure to build products on top of CBDCs. Once the banks build these capabilities, many use cases will emerge. Programmability of money is what I believe will drive the adoption of retail CBDC and target- linked money is a big use case,” said Neeraj Singh, co-founder of Xaults, which builds core banking solutions to help banks manage digital assets.

Read also | Digital Rupee: RBI plans to expand CBDC pilot to include more banks and locations

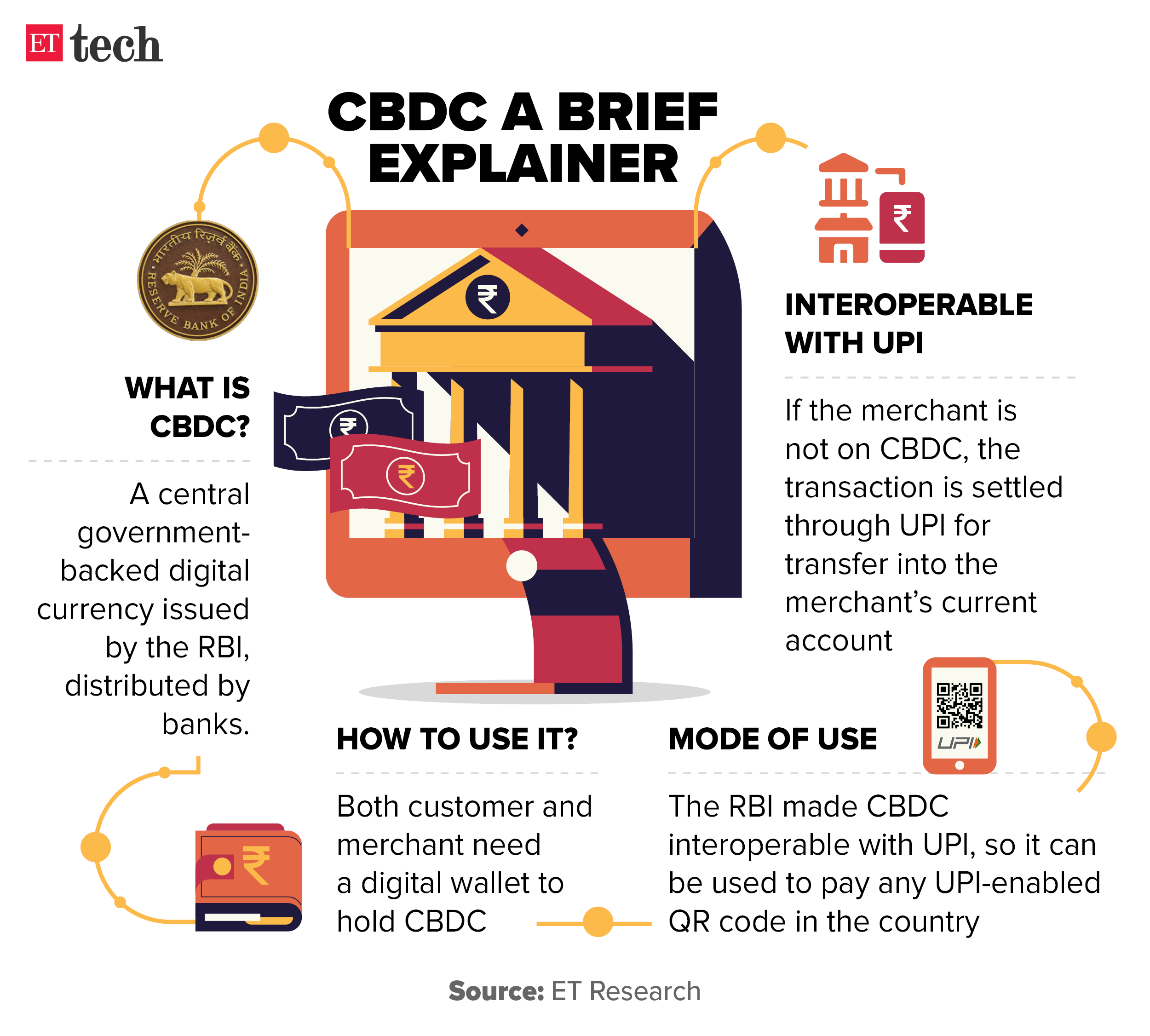

CBDC is a form of digital currency that is backed by the government, managed directly by the central bank and distributed by banks. Unlike private cryptocurrencies, which do not have the backing of any physical asset, this will be similar to sovereign money but in a complete digital format.

In December 2022, the RBI started a pilot program for retail adoption of CBDC in India. On November 24, banks are set to meet the RBI to discuss the progress of the pilot program.

Fall behind on goals

Currently, banks have three main goals: to build a customer base that adopts retail CBDC, to get merchants to accept CBDC and to hit a certain transaction volume on the platform.

The industry is lagging behind on all three goals, said one of the bankers quoted above.

Banks need to push for adoption so that the RBI can test the robustness of the CBDC ecosystem and ensure that the platform can scale up. News agency Reuters wrote in October that banks are being pushed to offer incentives to customers to drive adoption.

Person-to-person payments and merchant payments are already solved by UPI, hence consumers do not feel the need to adopt a new digital wallet for the same use case.

An experience similar to UPI

While UPI and the general digital payment adoption boomed during demonetisation and later Covid-19, such headwinds do not exist at present. So, it will need focused conscious drives.

Yes Bank, which is one of the initial banks participating in the RBI pilot program, is working on increasing customer awareness, said Ajay Rajan, country head, transaction banking.

“There are two important live use cases that we are currently trying to push forward. For consumers, CBDC transactions help declutter the savings account and make it more anonymous. Similarly, for merchants, settlement happens instantly compared to some other digital payment methods that happen with a delay,” said Rajan.

One section of the industry believes that the focus should be on areas where the transaction experience is not as smooth as consumer payments.

B2B payments or bulk transactions made between businesses is one such opportunity, believes Sharat Chandra, co-founder of India Blockchain Forum, a platform for crypto and digital currency enthusiasts.

“Hong Kong, Georgia, Australia and Singapore are some of the countries that have already shown CBDC use cases in real estate, capital markets, carbon credit trading and others. We need such initiatives in India as well,” said Chandra.

CBDC is still in the proof of concept stages with a few practical uses coming up here and there. It will take time to become part of the mainstream, like debit cards or UPI. When it does, a whole new world around digital currency will likely open up.