Concentrated lending links between non-bank financiers and major lenders can pose contagion risks, Reserve Bank of India (RBI) Governor Shaktikanta Das said, pointing to potential sectoral fault lines a week after the regulator sought to curb the recent rampant growth in unsecured advances. and to protect the wider financial system.

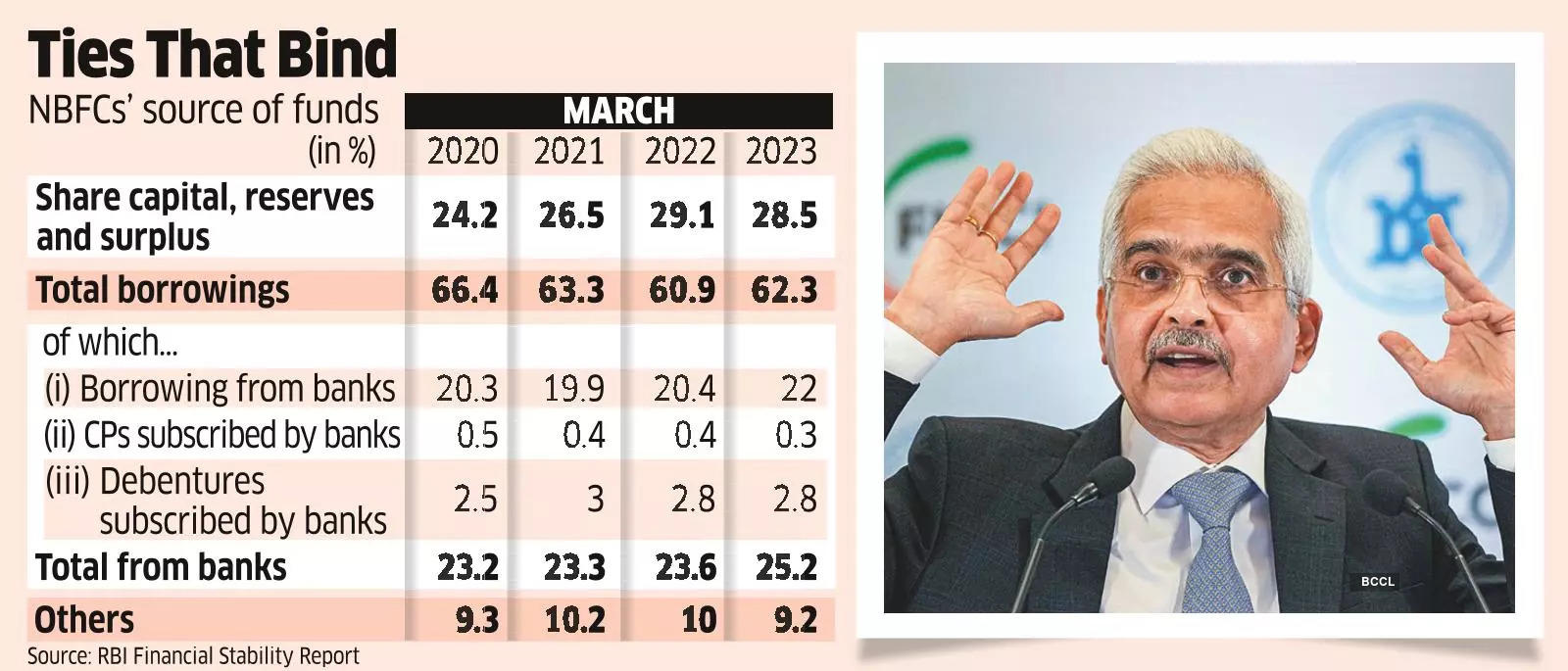

“NBFCs (non-banking finance companies) are large net borrowers of funds from the financial system, with their exposure from the banks being the highest,” Das told delegates at an industry conference on Wednesday. “Banks are also one of the major subscribers to the bonds and commercial papers issued by NBFCs. It goes without saying that such concentrated linkages can create contagion risk.”

He noted that NBFCs maintain lending relationships with several banks simultaneously. Therefore, banks must constantly assess their own exposure to NBFCs and the exposure of individual NBFCs to multiple banks, Das said.

NBFCs, on the other hand, need to focus on expanding their funding sources and bring down disproportionate dependence on bank funding, he said.

Sustainable credit

Non-bank lenders have played a crucial role in helping millions of Indians get on the consumer ladder for the first time, extending finance to help them buy modern gadgets, dream vacations, entry-level cars and even budget homes.

On November 16, RBI announced increases in bank capital requirements for consumer loans and ordered lenders to set limits on various retail segment loans, signaling the central bank’s vigilance over the rampant growth of these types of advances.

Das on Wednesday reinforced the message telling banks and NBFCs to ensure that credit growth at all levels remains sustainable and to avoid exuberance in any form. “The expansion of the credit portfolio itself and the price of the same should synchronize with the risks foreseen,” he said.

With the economy rapidly reopening following the easing of Covid-induced trade and mobility restrictions, bank credit growth has accelerated since April last year, even as deposit mobilization has followed the pace of credit expansion.

Emphasizing the need for prudence, Das urged banks and NBFCs to further strengthen their asset-liability management, especially on the liability – or deposit – side to avoid financial stress. “In some cases, we have observed an increased reliance on high-cost short-term wholesale deposits, while the holding of the loans, both in retail and corporate loans, is getting longer,” he said.

Look at abuse

Directly appealing to some NBFC microfinance institutions (MFIs) to shun “usurious” lending, the RBI governor told such financiers to keep in mind the affordability and repayment capacity of borrowers in this segment.

“Although interest rates are deregulated, some NBFCs-MFIs seem to enjoy relatively higher net interest margins. It is indeed for microfinance lenders to ensure that the flexibility provided to them in setting interest rates is used judiciously,” he said.

MFIs, which play a key role in financial inclusion, mainly serve marginalized and poor groups.

While cooperation between banks and fintechs has lowered operational costs, an area that deserves attention is related to model-based lending through analytics, Das said. Banks and NBFCs should be careful to rely only on pre-set algorithms, he said, demanding that models be robust, tested and re-tested periodically.

“There is a need to be careful about any undue risk build-up in the system due to information gaps in these models, which can lead to a dilution of insurance standards,” he said.

(tagsTo Translate)rbi