Growing pressure, from both social and political directions, has combined to boost clean and renewable energy providers, including residential-scale solar installations. Residential solar offers several benefits to the customer, including grid-independent home power and the ability to sell electricity back to the utility provider.

However, the residential solar business has faced strong headwinds in the last year or so, due to high interest rates increasing the cost of financing the installations. But with the Fed looking more likely to start lowering rates in the spring, some analysts see a brighter future for the residential solar sector.

Covering this business from Mizuho, analyst Maheep Mandloi looks at the industry’s prospects. “In 2024, we expect the industry to be dominated by: interest rate increases slowing (or reversing), the US Treasury clarifying the next phase of IRA rules, channel absorption of inventory in the first half, and increasing demand due to declining equipment costs,” Mandloi explained. “Residential (Resi) solar demand is expected to be under pressure until interest rates peak. However, we also see some room for increased value creation, as the adoption of energy storage increases the ticket sizes of renewable systems, and the costs of equipment fall against the background of higher electricity costs.

Building on his comments, Mandloi continues to monitor the residential solar industry, and picks two solar shares which have strong upside potential – well over 90%, according to the Mizuho forecast. Here are the details, pulled from the TipRanks databases, along with Mandloi’s comments.

Solar Nova Energy International (NEW)

The first residential solar company we will look at is Sunnova, a leader in the US market of this sector. Sunnova has its hands in all aspects of this niche, from setting up the rooftop solar panels to plugging into the home electrical system to installing the necessary electrical storage batteries. The company provides both installation and support services, and provides repairs, system modifications and spares and replacements to meet customers’ needs on demand. Sunnova can even provide financing options to smooth the way for customer purchases.

Sunnova was founded in 2012, and over the past decade it has expanded its operations into 47 US states and territories, from Arizona to Wisconsin. The company understands that every home is different, necessitating a custom approach to residential solar installations – but also helping to ensure customer-centric product delivery. From its Texas headquarters, Sunnova oversees the operations of its 1,900+ dealers, sub-dealers, and builders who serve the company’s 386,000+ strong customer base.

That customer base is growing, and at a solid clip. Sunnova added more than 39,000 new customers in 2Q23, and followed that up with more than 37,000 more in 3Q23. As of September 30 this year, Sunnova had 386,200 customers on the books, a figure that has increased significantly from the 279,400 reported at the end of 2022. Looking ahead, the company expects to bring in between 185,000 and 195,000 new customers during 2024.

That said, when we turn to the company’s recent earnings report, for 3Q23, we find that Sunnova missed expectations in its most recent quarter. Revenues came in at $198.4 million, up $49 million, or 33%, year over year — but still $3.6 million behind estimates. At the bottom line, Sunnova’s quarterly loss came to 53 cents per share by GAAP measures; this missed the forecast by 16 cents, and was a deeper loss than the 56 cents reported in the previous year.

Despite the recent earnings miss, analyst Mandloi still has an optimistic view of the stock. He particularly points to Sunnova’s strength in funding, as well as government support of last year’s Inflation Reduction Act (IRA). He writes, “Sunnova is among the leading residential solar finance companies in the US and has grown above the market growth rate since its IPO in 2019. We rate the stock Buy because of Sunnova’s ability to capture market share in an adverse environment as the industry shifts from loans to leases /PPAs, its increasing IRRs and value creation due to electric bill inflation coupled with a decline in equipment prices, its access to lower cost capital from DOE loan guarantees, high value potential from tax credit adders under the IRA, and an attractive valuation.”

Mandloi’s purchase rating is supported by a price of $20, suggesting that the stock will gain a robust 96% in the coming year. (To look at the history of Mandloi, Click here.)

There are no fewer than 20 recent analysts on Sunnova’s stock, reflecting the buzz that renewable energy can generate along with power. These reviews break down to 15 Buys and 5 Holds, for a Strong Buy consensus rating. The shares are selling for $10.22 and their $18.92 average price target implies 85% one-year upside potential. (See Sunnova’s stock forecast.)

Sunrun, Inc. (RUN)

The second stock on our list is Sunrun, another leading company in the US residential solar energy market. Sunrun bills itself as a full-service provider, with a focus on custom customer solar installations for single-family homes. This niche once meant “rooftop solar panels,” but the technology and aesthetics are far more advanced than the simple panels that former President Jimmy Carter put over the White House in the 70s. Sunrun designs, builds and installs high-quality packaged solar offerings, tailored to each customer’s home.

Included in the package deals are, of course, rooftop photovoltaic panels, as well as grid connections, “smart” control systems and high-tech power storage batteries. The company will also offer financing and multiple payment options. Customers can choose options to pay in advance, in full, or set up a payment plan based on long-term amortization with equipment lease and monthly payments.

Financial flexibility has helped push Sunrun into the upper echelon of residential solar. The company brought in 33,806 new customers in 3Q23, of which 29,303 paid subscriber additions. The company’s net subscriber value was $11,030 through the third quarter.

Sunrun’s earnings hit a recent peak in the second half of last year, and have declined somewhat since then. The current trade headwinds, including high interest rates, have caused a slowdown in business. The prospect that interest rates could follow inflation down in the first quarter of next year is bullish for a company dependent on customer financing.

And this brings us to Mandloi’s view of RUN, which is bullish – in part because the company is already using a rent-based long-term payment mode, which he sees as growing more important going forward. Mandloi sums up his view of Sunrun in a recent note, writing, “Sunrun is the largest third-party owner and developer of residential solar systems in the US. We are rated Buy because of Sunrun’s leadership in the US residential market, where it is gaining market share in an adverse environment as the industry shifts from loans to leases/PPAs, its improved value creation due to electric bill inflation coupled with a decline in equipment prices, top of tax credits under the IRA, and attractive. valuation despite higher interest rates.”

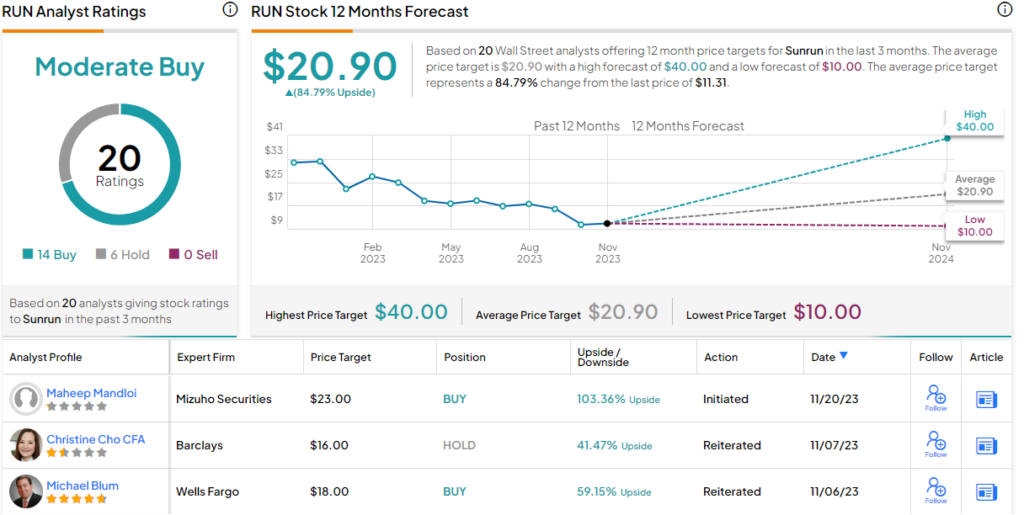

The aforementioned Buy rating is accompanied by Mandloi’s $23 price target, which implies a strong 103% upside potential for the next 12 months.

The rest of the Street is mostly on board, too. The Moderate Buy consensus rating on the stock is based on 20 ratings, of which 14 are Buy compared to 6 Hold. The average target price of $20.90 suggests an upside of 85% from the current trading price of $11.31. (See Sunrun’s stock forecast.)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that brings together all the stock insights from TipRanks.

Disclaimer: The opinions expressed in this article are solely those of the prominent analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.