MUMBAI: Banks have started questioning the “source” of money that individuals move abroad, especially to acquire properties abroad.

Sometimes they scan past income statements to find out the origin of the fund while some banks recently asked if the money that would be transferred out of the country was a “gift” from a relative.

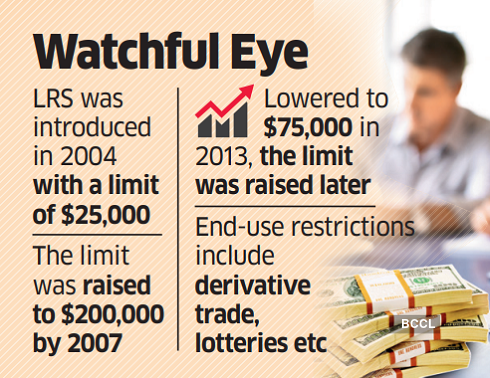

Under the Liberalized Remittance Scheme (LRS), resident individuals are allowed to transfer up to $250,000 per year abroad to invest in properties and securities, maintenance of relatives, among other specified purposes. Some of the tax professionals and bankers ET spoke to said authorized dealer (AD) banks undertake greater scrutiny before clearing LRS consignments.

“Many residents have been using the LRS to send funds since 2004. Similarly, non-resident Indians have been sending money under the regulations allowing them to transfer a million dollars a year from India. However, recently, many AD banks are withholding remittances, citing internal instructions that is not in the public domain or part of any regulation or master direction. It would be helpful if there is greater regulatory clarity on what is allowed and what is not,” said Rajesh P Shah, partner at Jayantilal Thakkar and Company, a chartered accountancy firm specializing in tax and matters related to the Foreign Exchange Management Act (FEMA). Total remittances under LRS rose from $12.68 billion in 2020-21 to $27.14 billion in 2022-23, after dipping to $19.61 billion in 2020-21. According to available figures released by the Reserve Bank of India (RBI), which regulates the scheme, remittances crossed $27.4 billion for the April-January period of 2023-24.

At least two private banks (one large AD, another mid-sized) have recently questioned clients about the fund source, sources said. Banks, probably sensing the current regulatory environment, feel that some are using the LRS window for purposes for which it was not originally intended.

“The original interpretation of the liberalized remittance scheme was to ensure that all funds sent for capital or current transactions belong to the remitter (personal savings, education loan, salary, business income, as mentioned in form A2). Based on the RBI guidelines. , the AD bank has the power to check and even question the source of funds (more especially for property or capital transactions) and ask for supporting documentation like bank statements, tax returns etc.,” said Priyanshi Chokshi of Adarsha Advisors who offers tax. and international accounting services.

However, there are multiple scenarios where individuals send funds as follows: cash gift provided by father to son is further transmitted, use of borrowed funds, use of funds obtained by financing an individual’s own company, said Chokshi. “The AD banks are now scrutinizing such transactions more closely, in line with RBI’s intent to ensure that a sender uses funds ‘belonging to him’ and does not send the funds for illegal or laundering purposes,” she said.

However, such “gift” remittances are primarily a mechanism to pool adequate family funds to purchase property abroad. In certain cases, such investments are a precursor to migration to countries with programs offering citizenship in exchange for investments.

“Requesting source details is not an order according to the LRS standards. Such inquiries are more guided by the internal policies of the bank or in connection with any account-specific issues. It serves as a check whether the limits set below the limits. LRS are not exceeded directly or indirectly ,” said Yashesh Ashar, a partner at Illume Advisory engaged in services such as accounting, taxation and corporate finance. For example, a person who has already exhausted his annual LRS limit can ask a relative to send the money on his behalf.