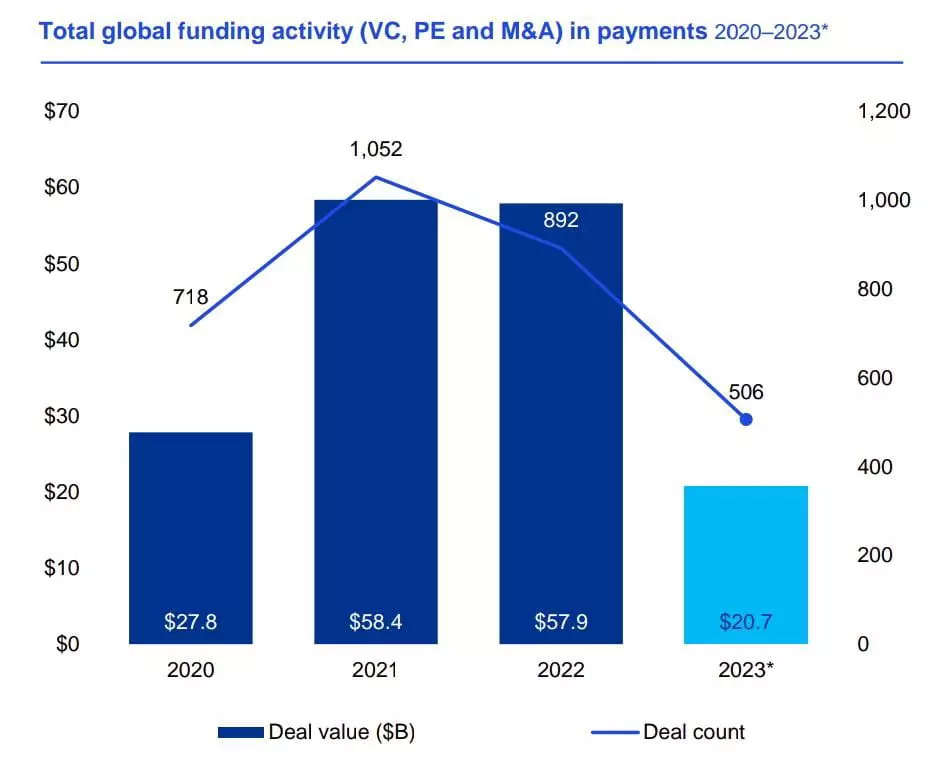

Despite a significant decrease in annual investment – from USD 58 billion in 2022 to USD 20.7 billion in 2023 – and the number of deals – from 892 to 506 – the payments space continued to account for the largest share of fintech investment worldwide, revealed last . report by KPMG.

In H2’23 there was a clear retreat in mega deals with two billion dollar deals: Finastra – USD 6.9 billion and Pismo – USD 1 billion. In comparison, H1’23 saw four payment deals greater than USD 1 billion (ie Stripe – USD 6.9 billion, EVO Payments – USD 4 billion, Moneygram – USD 1.8 billion, and Paya – USD 1.3 billion).

Source: KPMG Pulse Of FinTech Report

Source: KPMG Pulse Of FinTech ReportDespite a significant decline in deal value, the M&A space remained quite active during the second half of the year as a result of ongoing global, regional and local consolidation efforts across companies focused on providing core payment platforms and related services, the report emphasized.

Merger activity accounted for three of the six largest payments deals during 2023, including the $4 billion acquisition of US-based EVO Payments, the $1.3 billion acquisition of Paya and the $1 billion acquisition of Brazil-based Pismo.

SOURCE: KPMG Pulse Of FinTech Report

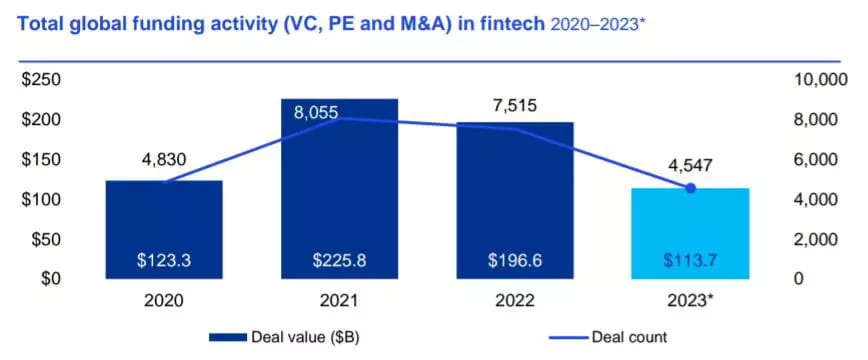

SOURCE: KPMG Pulse Of FinTech ReportWhile M&A activity slowed in H2’23, interest in consolidation and M&A remained quite high due to the pressure for companies to improve their product sets to become more profitable and continue to grow their reach geographically, the report said.

Deal sizes are shrinking considerably

The USD 6.9 billion raised by Stripe in H1’23 accounted for more than the total global investment seen across the payments space in H2’23, highlighting the significant reduction in payment deals, the KPMG report highlighted.

Visa’s USD 1 billion acquisition of Brazil-based payment processing and banking platform Pismo was the biggest deal of H2’23, followed by the USD 385 million buyout of Finland-based cash management software company Nomentia by UK-based PE -company Inflexion, and the USD. 275 million VC raise of US consumer credit card company Petal.

The report further highlighted that payment processing continues to be a significant priority of investors, increasing investment in the B2B payment space, including real-time payments and BNPL, increasing focus on partnerships in the embedded payment space, large BNPL companies focusing on geographic, product. and partnership diversification and expanding investments across jurisdictions as macroeconomic conditions improve are some trends to watch for in the first half of 2024.