The New India Assurance Co. Ltd, India’s largest public sector general insurance company, lags behind its largest private sector peer ICICI Lombard General Insurance in terms of market capitalization.

The latest market capitalization of New India Assurance and ICICI Lombard stands close to ₹43,500 crore and ₹80,700 crore, respectively. This is although the market share of the former is at 16% against about 8% of the latter.

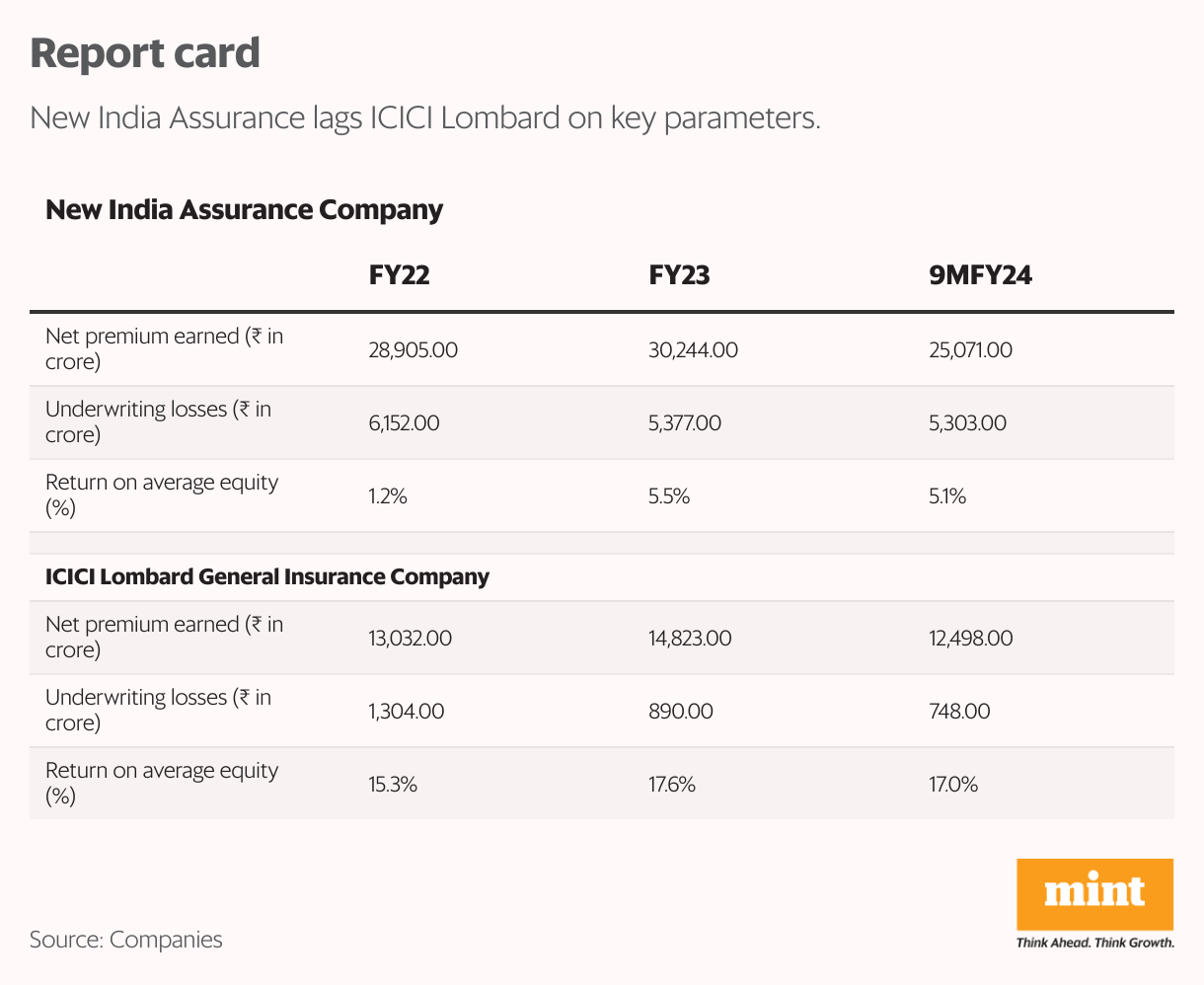

A deep dive into the comparative finances of the two reveals the reasons.

To begin with, New India Assurance’s underwriting losses are much higher than ICICI Lombard. For example, in the December quarter (Q3FY24), New India’s underwriting loss was at ₹1,390 crores. Underwriting loss is calculated by deducting the claims made and operating expenses from the net premium earned (or simply put: income). It indicates the insurance standards, or in other words, it is the risk assessment ability of an insurer regarding the likelihood of a claim when insuring a person, object or property.

Certainly, it can be argued that ICICI Lombard also reported an underwriting loss of ₹280 crore last quarter, but the loss as a percentage of net premium earned is much lower at 6.5% against 15.5% for New India Assurance.

New India Assurance still managed to report an operating profit of ₹290 crore on account of investment value income ₹1,680 crores. Operating profit is the sum of underwriting profit/loss and income from investments. The reason for the underwriting loss was that New India Assurance had to pay almost 93% of the net premium earned towards claims. Even though the claims related to catastrophic losses due to the cyclone and floods in South India, Sikkim, and West Bengal are worth ₹350 crores are excluded, the ratio comes to 89%. This is much higher than the 70% reported by ICICI Lombard in Q3FY24.

Further, ICICI Lombard enjoys a higher solvency ratio of 2.57 against New India Assurance’s 1.72. The higher solvency ratio indicates the ability to underwrite more business or do more business selling new insurance. ICICI Lombard has maintained return on equity (RoE) over 15% for the last three years. New India Assurance is far from clocking a double-digit RoE in the near future. In the nine-month period ended December, its RoE stood at 5.1% and in FY23, it was at 5.5%.

Despite the higher base, New India Assurance did a good job of matching ICICI Lombard’s net premium earned or top-line growth rate at 14% in Q3. However, New India Assurance has a long way to go to catch up with its private peer in terms of profitability.

Having said all this, it is not surprising that ICICI Lombard commands a market capitalization of ₹84000 crore which is almost 2x that of New India Assurance. While the net worth or book value of New India Assurance is at ₹20000 crore, almost double that of ICICI Lombard, it is clear that the market is valuing the stock based on the quality of earnings and RoE rather than simply the price to book value multiple.

Going forward, growth is unlikely to be a challenge for New India Assurance and the industry at large, as non-life insurance in India is about one-fourth of the global average according to a Swiss Re report. However, investors should monitor the progress of New India Assurance’s future strategy to increase RoE by rationalizing office and related costs along with growth through digital penetration.

Certainly, until about six months ago, New India Assurance was deeply undervalued with its market capitalization well below its net worth. Investors noticed this when shares of all public sector units (PSUs) started rallying after Prime Minister Narendra Modi made a statement in Parliament on improving governance in government companies. The result is that over the past one year, New India Assurance shares have risen more than 150% against ICICI Lombard’s roughly 50% gain over the same period. ICICI Lombard also fared well after ICICI Bank, its parent, increased its stake following the Reserve Bank of India’s nod to do so to 4%.