Reigns Supreme within the Streaming Kingdom")

Netflix stock (NASDAQ:NFLX) reigns supreme in the vaping realm, with its most recent results showing continued industry dominance. With more than 260 million paid members, the streaming giant continues to post robust growth in revenue and earnings despite the industry suffering from oversaturation. In fact, improved profitability has enabled management to return significant capital to shareholders, enhancing the stock’s appeal. I believe that this trend is to be continued. Thus, I am bullish on NFLX stock.

Subscriber Growth Accelerating Against All Odds

Netflix continues to amaze with its remarkable ability to consistently attract paid subscribers, even with the fierce competition in the saturated streaming and social media space. In an age where tech and media giants are fighting for consumers’ attention, the company’s continued subscriber growth is nothing short of amazing.

Think about that for a minute. The streaming and social media space is more saturated than ever, with many players fighting for viewers’ precious viewing time. At first, Netflix dominated the space, mainly by going up against outdated cable networks. However, the dynamic has changed, and Netflix is now struggling with a host of streaming services, including Disney (NYSE:DIS) Disney+, Amazon (NASDAQ:AMZN) Prime Video Service, AT&T’s (NYSE: T) HBO, Hulu, Peacock, and various smaller players.

In addition, Netflix faces competition in the “attention economy” from tech giants like Alphabet’s (NASDAQ:GOOGL), YouTube, TikTok, and Meta Platforms’ (NASDAQ: META) Coils. They are all striving to capture market share in audience to increase their advertising revenue. In fact, TikTok and Reels’ focus on promoting both short-form and long-form views and even producing shows on their own is evidence of their competition with Netflix.

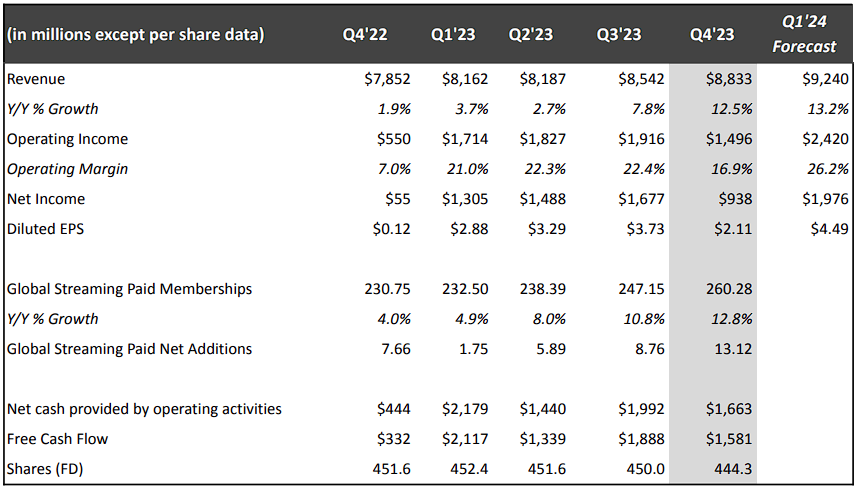

Despite these challenges, Netflix maintains a robust subscriber base, and its paid subscriber growth has even accelerated in recent quarters, including its latest Q4 results. To illustrate, here are Netflix’s quarterly paid subscribers over the past two years.

- Q1 2022: 6.7%

- Q2 2022: 5.5%

- Q3 2022: 4.5%

- Q4 2022: 4.0%

- Q1 2023: 4.9%

- Q2 2023: 8.0%

- Q3 2023: 10.8%

- Q4 2023: 12.8%

These figures clearly show a moderation in paid subscriber acquisition during 2022, after the unprecedented growth of subscribers during the previous two years. The widespread stay-at-home trend during the pandemic stimulated remarkable growth in 2020 and 2021, and Netflix experienced a remarkable 20% increase in paid memberships during that period. Therefore, a slowdown in growth for the following year, 2022, was predictable as the situation began to stabilize.

However, as conditions normalized, subscriber growth rebounded significantly in 2023, showing a notable increase on a quarterly basis. The most recent quarter’s growth of 12.8% is particularly noteworthy, pushing Netflix’s paid subscriber base to a staggering 260.3 million.

Revenues and Earnings Increase, Outlook Looks Very Promising

Powered by an acceleration in subscriber growth, revenue growth also followed a similar trend. The same applies to earnings, as margins have increased, and the income statement benefits from an improvement in unit economics. In the meantime, Netflix’s outlook for the first quarter of 2024 suggests that this trend will continue.

To illustrate, Netflix posted record revenues of $8.54 billion in Q4, a year-over-year increase of 12.5%. As you can see in the table below, revenue growth has also accelerated, in line with subscriber growth. Notably, this increase was the best for the company since the Q4-2021 growth rate of 16%. At the same time, NFLX’s operating margin jumped to 16.9%, notably higher than last year’s 7.0%. This combo allowed net income and EPS to rise to $938 million.

Also of note is the fact that Netflix’s share count fell 1.6% to 444.3 million, with management deploying just over $6.0 billion in buybacks in Fiscal 2023. While not a massive drop, management’s clear intent to increase buybacks should translate to gradually accretive effect on earnings per share, which is welcomed.

But in addition to closing the year on a high note, investors were particularly impressed with management’s Q1-2024 outlook, which shows further revenue acceleration and a significant expansion of revenue margin expansion. In particular, revenues are expected to grow by 13.2%, while operating income margin is expected to reach 26.2%, which implies a remarkable expansion from last year’s 21% and last quarter’s 16.9%.

Is NFLX stock a buy, according to analysts?

As for Wall Street’s view of Netflix, the stock has drawn a consensus rating of Moderate Buy based on 27 Buys, 13 Holds and one Sell assigned in the last three months. At $574.01, the average Netflix stock forecast implies a 2.6% upside potential.

If you’re wondering which analyst you should follow if you want to buy and sell NFLX stock, the most profitable analyst covering the stock (on a one-year time frame) is Oppenheimer’s Jason Helfstein, with an average return of 43.42% per estimate. and 100% success rate. Click the image below to learn more.

The Takeaway

Netflix’s unrelenting dominance in the streaming realm remains impressive, defying industry saturation and intense competition. The recent boost in paid subscribers and growing revenue and earnings paint a promising outlook for the future. With sensible rising share buybacks and optimistic goals from management heading into 2024, Netflix stock seems positioned for continued success in 2024.

Disclosure

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.