to Your Portfolio Proper Now")

TransAlta Corporation TAC continues to benefit by providing safe, reliable and clean energy to its customers. Given its growth opportunities, TAC makes a solid investment choice in the service sector.

Let’s focus on the factors that make this current Zacks Rank #2 (Buy) company a strong investment choice at this time.

Growth Projections & Surprising History

The Zacks Consensus Estimate for 2024 and 2025 earnings per share (EPS) is set at 51 cents and 53 cents, respectively. The consensus estimate for 2024 and 2025 EPS rose 10.9% and 29.3%, respectively, in the past 60 days.

The company delivered an average earnings surprise of 142.6% in the last four quarters.

Return on Equity (ROE)

The metric indicates how effectively a company has used the funds to generate higher returns. Currently, TransAlta’s ROE is 48.42%, higher than the industry average of 10.26%. This indicates that the company used the funds more constructively than its peers in the electric utility industry.

Dividends and share buyback

The company has consistently increased its shareholder value by paying dividends and by repurchasing shares. TAC has paid dividends 13 times in the past five years. Its current dividend yield is 2.41%, better than the Zacks S&P 500 Composite average of 1.58%.

TransAlta’s management announced an enhanced common share repurchase program for 2024 of up to $150 million toward the repurchase of common shares. The company plans to return nearly 40% of its free cash flow to shareholders in 2024, through dividends and share buybacks.

Liquidity and Financial Position

As of December 31, 2023, TransAlta had access to $1.7 billion in liquidity, including $345 million in cash, net of bank overdraft, which significantly exceeds the funds needed for committed growth, continuing capital and productivity projects.

The company’s time-interest-earned (TIE) ratio at the end of 2023 was 4.1. The strong TIE ratio also indicates that the company has enough financial strength to meet its interest burden.

Development Plans

The company aims to add 10 Gigawatts of new assets to its portfolio by 2028 and invest $3.5 billion to reach its production target.

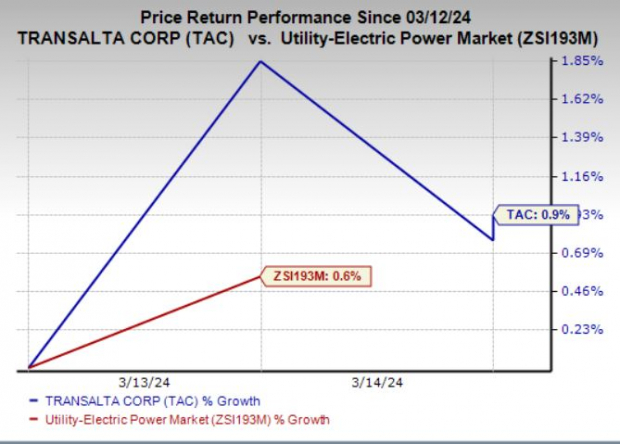

Price Action

In the past two days, the company’s shares gained 0.9% compared to the 0.6% growth of the industry.

Image source: Zacks Investment Research

Other Stocks to Consider

Some other top ranked stocks from the same industry are DTE Energy DTE, Unitil Corporation UTL and WeSource WE, each currently carrying a Zacks Rank of 2. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

DTE’s long-term (three to five years) earnings growth rate is 6%. The Zacks Consensus Estimate of 2024 EPS of $6.70 has risen 0.5% in the past 60 days.

UTL’s long-term earnings growth rate is 7.1%. The Zacks Consensus Estimate of 2024 EPS of $6.70 has risen 0.4% in the past 60 days.

NI’s long-term earnings growth rate is 7.2%. It delivered an average surprise of 5.6% in the last four quarters.

7 Best Stocks for the Next 30 Days

Just released: Experts distill 7 elite stocks from Zacks Rank #1’s current list of 220 Strong Buys. They deem these typewriters “Most Likely for Early Price Pops”.

Since 1988, the full list has beaten the market more than 2X with an average gain of +24.2% per year. So be sure to give these handpicked 7 your immediate attention.

See them now >>

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

NiSource, Inc (NI): Free Analysis Report

DTE Energy Company (DTE): Free Analysis Report

TransAlta Corporation (TAC): Free Analysis Report

Unitil Corporation (UTL): Free Analysis Report

To read this article on Zacks.com click here.

Zacks Investment Research

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.