Finance Minister Nirmala Sitharaman has asked regulators to hold monthly meetings with startups and fintech firms to address their issues and concerns while emphasizing strict regulatory compliance.

Sitharaman met startup and fintech stakeholders on Monday along with senior government officials.

The much-awaited meeting comes amid the Reserve Bank of India’s actions against Paytm Payments Bank (PPBL).

The finance ministry outlined six action points after the meeting, which was also attended by RBI deputy governor T Rabi Sankar, State Bank of India chairman Dinesh Kumar Khara and officials of the National Payments Corporation of India (NPCI), among others.

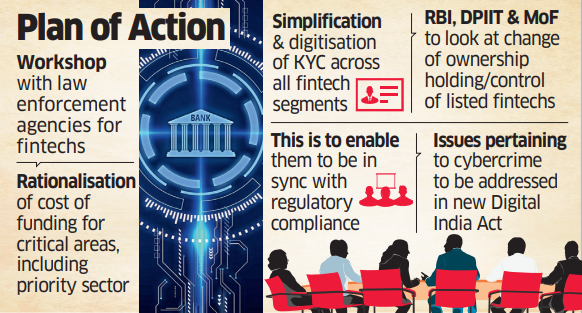

These action points include simplification and digitization of KYC (Know Your Customer) across all fintech segments and interaction with law enforcement agencies to allow fintech companies to voice their issues or concerns.

Cybercrime issues will be adequately addressed in the new Digital India Act, the finance ministry said in a statement after the meeting.

“RBI, DPIIT (Department for Promotion of Industry and Internal Trade) and MoF (Ministry of Finance) to look into the change of ownership ownership/control of listed fintech companies to enable them to be in sync with regulatory compliance,” according to the statement.

Last week, ET reported that Sitharaman will meet heads of fintech firms in the backdrop of RBI’s action against PPBL.

Meanwhile, Vijay Shekhar Sharma resigned on Monday as part-time chairman and board member of PPBL. PPBL is an associate unit of One 97 Communications Ltd, the parent company that owns and operates the Paytm brand.

“Sitharaman has advised the regulators, including RBI, that they may hold meetings through virtual mode once a month to discuss any questions, queries or concerns of the startups and fintech companies,” the ministry said in the statement.

No anxiety or concerns related to Paytm were shown by the startup founders or fintech entities during the meeting, an official said.

On January 31, the RBI asked PPBL to stop accepting deposits, credit transactions or top-ups in any customer accounts, prepaid instruments, wallets, FASTags, and National Common Mobility Cards, after February 29. The deadline was later extended to the March 15th. .

A group of founders later wrote a letter to finance minister and RBI governor Shaktikanta Das, asking the regulator to reassess “the proportionality of restrictions, given their potential impact on Paytm Payments Bank, the fintech ecosystem and the wider economy”.

Sitharaman noted that India’s fintech ecosystem is the third largest in the world and is growing at 14% CAGR and that the central bank recently presented a draft framework for Self-Regulatory Organization (SRO) recognition for the sector for stakeholder consultation. , the statement said. .

“The number of startups in India has grown significantly from just over 300 in 2016 to over 1.17 lakh in 2023 as recognized by DPIIT, generating over 12.4 lakh jobs, and 47% of the startups have at least one woman director,” the statement. noted

“DFS will conduct a one-day workshop with Law Enforcement Agencies (LEAs) in which fintech ecosystem partners can voice their issues or concerns.”

The discussions were a two-way dialogue where the fintech industry expressed its concerns on operational aspects such as KYC, consultation on the digital protection of personal data bill and on the goods and services tax (GST), an industry executive said.

“One important topic that the industry proposed was about common KYC for fintechs. The ministry was receptive to the suggestions made by the participants and asked the industry to send a letter for the government to take it,” added the executive.