Inventory")

While the stock markets made a remarkable comeback in 2023, several individual stocks are down this year. One such stock is the retail footwear company Crocs (NASDAQ:CROX). Valued at a market cap of $5.7 billion, CROX shares are down nearly 50% from all-time highs. While investors remain wary of the mid-cap company, I am bullish on its attractive growth prospects, widening profit margins and very cheap valuation.

CROX’s Stock Falls Following Q3 Report

Crocs is the company behind iconic brands like HEYDUDE and, of course, Crocs. While it is part of the mature retail footwear market, Crocs has grown its revenue from $1.23 billion in 2019 to $3.55 billion in 2022.

In Q3 2023, Crocs reported revenue of $1.05 billion with adjusted earnings of $3.25 per share. Analysts forecast that the company will report revenue of $1.03 billion and earnings of $3.10 per share. But after its Q3 results on Nov. 2, Crocs shares fell more than 5% as investors were unimpressed by its 2023 guidance.

Crocs estimated revenue between $3.905 billion and $3.94 billion for 2023 compared to a consensus forecast of $4.01 billion. Its earnings guidance of between $11.55 and $11.85 per share was also lower than estimates of $12.09 per share.

However, in Q3, Crocs surpassed the top line of its revenue guidance due to double-digit revenue in its Crocs brand. Its top line was buoyed by industry-leading operating margins as the company gained market share amid the back-to-school season.

HEYDUDE Brand Under Focus

Crocs completed the acquisition of HEYDUDE for $2.5 billion in early 2022. While the company generates revenue from multiple channels such as Direct-to-Consumer, Wholesale, and Retail, HEYDUDE’s primary source is from its wholesale distribution channel.

In Q3 2023, Wholesale revenue for HEYDUDE fell by 19.4%, spooking investors in the process. The company now aims to accelerate its marketing management strategy to ensure long-term growth, resulting in a readjustment of its full-year outlook.

Three Reasons CROX Stock is Attractive

Despite the discontinued sale of Crocs’ HEYDUDE brand, the retail stock remains an attractive investment option. Let’s see why.

1. The Stock is Undervalued

Crocs expects to increase its revenues at an annual rate of 10% in the next five years. Currently priced at 7.8x forward earnings, CROX is cheap and trades at a PEG (price-to-earnings-growth) ratio of 0.87x. Generally, a PEG ratio of less than one indicates that a stock is undervalued.

2. Profit Margins Improve

As a standalone brand, Crocs reported an operating margin of 37.4% in Q3 compared to 33.1% in the year-ago period. Because of its improving bottom line, Crocs reduced its corporate debt by $400 million to $1.9 billion in the last three quarters. It also provided Crocs with the flexibility to buy back shares worth $150 million in Q3.

3. HEYDUDE Sales Should Normalize

Shortly after the acquisition, Crocs aggressively flooded the market with HEYDUDE products, resulting in higher inventory levels. Basically, Crocs wanted to increase brand awareness for HEYDUDE and is now struggling with the growing pains associated with the brand.

Crocs expects HEYDUDE sales to decline by at least 20% in Q4 2023, resulting in single-digit growth for the combined entity.

However, Crocs expects HeyDude to hit $1 billion in sales in 2024, which suggests its sales estimates for the next 12 months may move significantly higher.

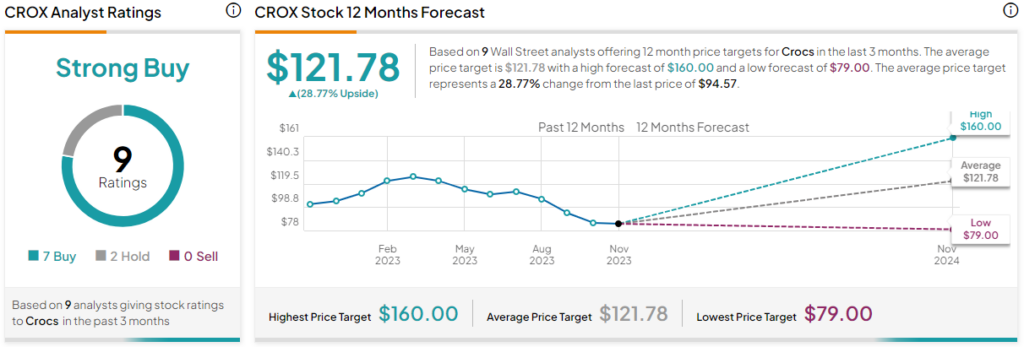

Is CROX Stock a Buy, According to Analysts?

As for Wall Street’s view of the stock, Crocs presents a consensus rating of Strong Buy based on seven Buys and two Holds assigned in the past three months. At $121.78, Crocs’ average share price implies an upside potential of 28.8%.

Conclusion

It’s entirely possible that the market is overlooking Crocs’ dirt cheap valuation and solid sales and profit margin growth. With CROX stock very high, it allows investors to accumulate shares at a discount and likely benefit from large gains when market sentiment recovers.

Disclosure

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.